Summers are often a very strategic quarter, and this summer is no exception. Our reading of the tea leaves suggest that Snowy Hydro is successfully keeping NSW spot prices contained, to leverage their position.

In NSW, there have been 5 days in the first quarter of this year when spot prices have threatened to reach extreme levels. Without exception, each day Snowy Hydro has offered 2,000 to 3,000MW of capacity below negative $500/MWh. This price point ensures the offers are accepted and thereby puts downward pressure on price. The strategy has been highly successful, as only a few spot prices have popped through to extreme levels.

Let's have a look at what happened, and then we can speculate why?

What happened?

The five days of summer when NSW spot prices threatened to reach extreme levels were:

- Tuesday 1 February when Sydney and Brisbane both had a hot day (31.7 and 34.2 degrees respectively), combined with several outages

- Thursday 17 February

- Tuesday 22 February

- Monday 7 March

- Tuesday 8 March when Brisbane had a hot day reaching 34.2 degrees, although Sydney was only 22.4 degrees

The interactive chart below shows for each of the five days, the offers from Snowy Hydro and the half hour spot price. This analysis has been performed at half-hour level, even though 5-minute settlement has been in operation since 1 October 2021 which means 5-minute spot prices and 5-minute generation determine cash flows for market participants. The purpose of using 30-minute data here, is to show the messages, rather than the detail.

By using the drop-down list for each day, you can view the capacity offered by Snowy Hydro for each half hour of each day. The capacity is categorised into bands of prices to enable easy presentation of the results. You can note the dark grey represents capacity offered below -$500/MWh. Snowy's offers in this below -$500/MWh price band was significantly between 2,000 and 3,000MW each time the spot price threatened to reach extreme levels.

You are welcome to step-through each day using the drop down, and you will see that only on a few occasions did prices begin to run-away from Snowy's apparent strategy of suppressing price.

We speculate why?

One can only speculate why Snowy Hydro wished to suppress prices, so these comments are purely our reading of the tea leaves.

If we go back to the Senate hearing held on 14 February 2022 when Mr Wymer, the Chief Commercial Officer of Snowy Hydro stated "As a guide, our futures book, the number of contracts that we have open, since Q1 2020 to Q1 2022 multiplied by five. It went from 700 megawatts to 3,500 megawatts."

Following the Senate hearing comment, it seems reasonable to presume Snowy Hydro has sold a lot of $300/MWh caps which means if the price exceeds $300/MWh, then Snowy Hydro would pay the buyer the difference between the spot price and $300/MWh. In return for this insurance product, the buyer would pay a premium for the protection.

If Snowy Hydro is dispatched for the cap quantity sold then Snowy would simply receive the spot revenue, keep the value below $300/MWh, and then payout the value above $300/MWh. However, if Snowy sold more than was able to be dispatched, then Snowy would pay-out the value above $300/MWh for the additional quantity sold, with no spot revenue stream to draw from. In energy trading speak, this is holding a short trading position.

What about leveraging the strategy? If Snowy sold more $300/MWh cap capacity than the expected dispatch levels, then provided Snowy can contain the price to remain below $300/MWh, then no payout would be triggered. The premium paid for the entire quantity sold would be retained. Looking at the actions of Snowy Hydro, our tea leaf reading suggests this is the case.

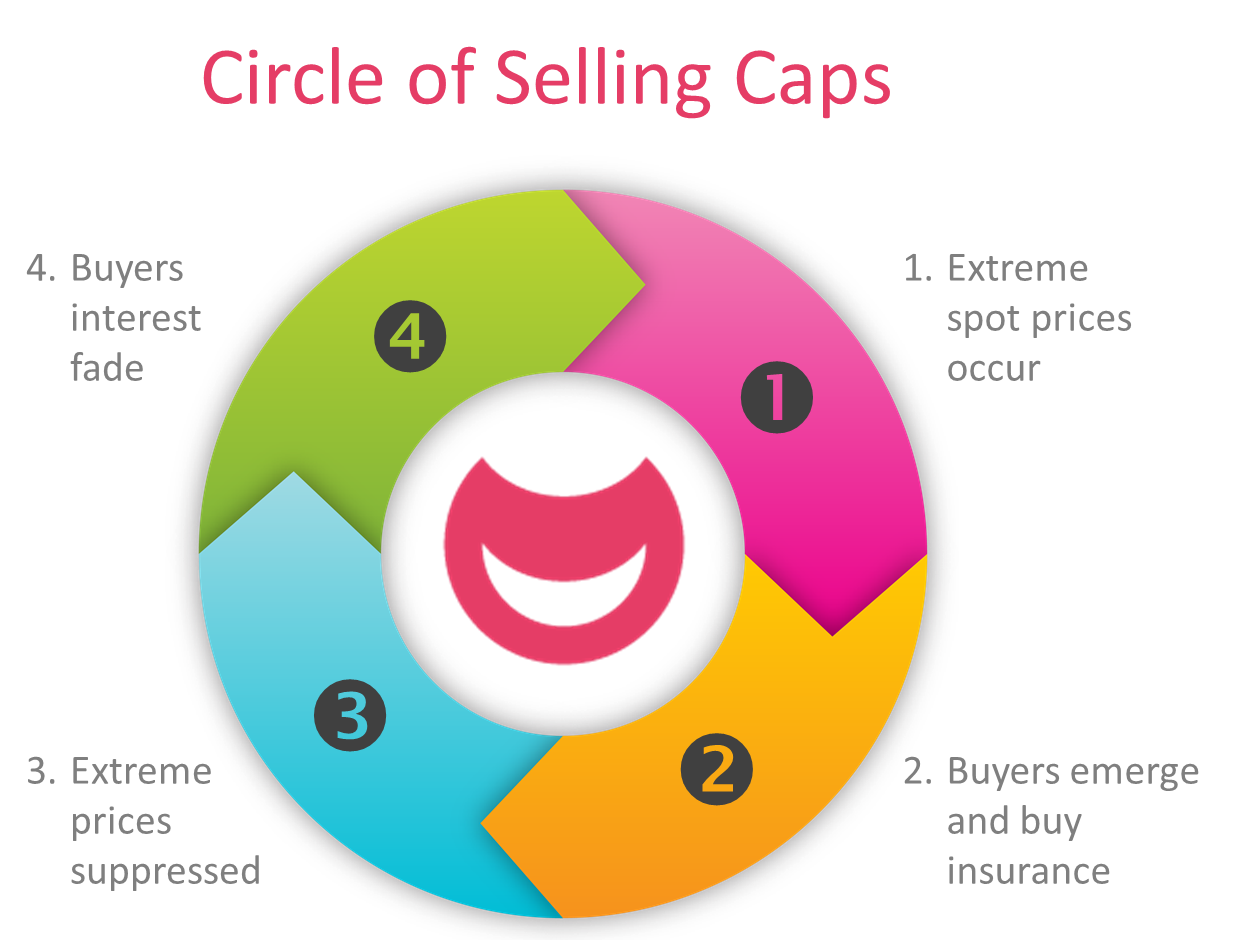

Circle of Selling Caps

Risk management products like $300/MWh caps operate on Buyer's fear (or risk management limits), that extreme prices may become rampant and thereby cause financial stress (sometimes fatal). However, if the apparent behavior from Cap Sellers becomes 'bankable', then the Buyer will conclude they do not need to buy any insurance product, because the Sellers will contain the price anyway. In such a scenario, the Buyers fade away and the interest in buying $300/MWh caps fade.

The Seller then faces less interest from Buyers, so shifts the strategy from suppressing prices, to letting the extreme prices run. Sufficient financial pain inflicted will then draw Buyers back into the market, and then the cycle starts again. Perhaps this phenomenon should be called the 'Circle of Selling Caps'.