The summer of 2024 has begun, and the month of January has set records at two ends of the spectrum.

In sunny Queensland, the pavements were too hot for bare feet as high temperatures and humidity drove demand to unprecedented levels and consequently pulled market spot prices to extreme levels. Before the quarter commenced, the Q1-24 base load contract was trading at $116/MWh, but then after the Australia Day long weekend peaked at $146/MWh. Since this peak, the market has softened to $136/MWh.

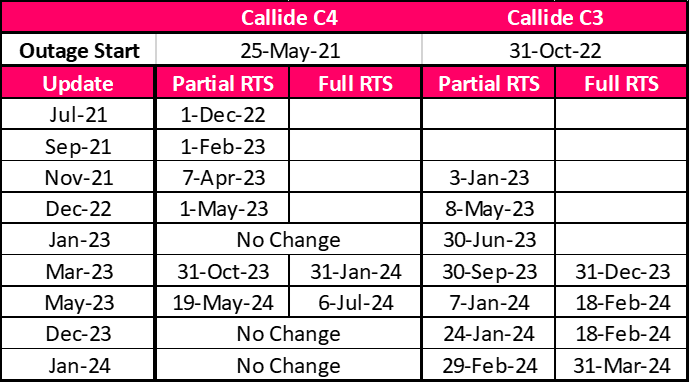

To add to the Queensland story, the long-awaited return of Callide C units, both of which have received numerous return-to-service (RTS) updates, was delayed and now the C3 unit is not due back until 29 Feb-24 and C4 unit is due to return on 19 May-24. The history of the outage and return-to-service announcements is shown in the table below:

The Queensland January spot price was $160.43/MWh, the second highest on record; beaten only by 2017 at $197.65/MWh.

At the other end of the spectrum, Victoria which was meant to have the summer-of-all-summers, has so far been a non-event. The January average spot price was $22.10/MWh, the lowest January average in history. The chart below shows the historical average spot prices since the markets began.

In anticipation of a hot summer, the Victorian forward price before the quarter started was $66.75/MWh after softening from the December peak of $73.75/MWh. Today, the forward market price has slipped to $36.05/MWh, less than half the December peak level.

The chart below shows the daily maximum temperature for Brisbane and Melbourne and clearly demonstrates that Brisbane has experienced hot weather, while Melbourne has had only 4 days above 30 degrees.

It is remarkable how the market continues to evolve, although like any change, bumps in the road occur. Seven daily prices during the Victorian month averaged below zero in January. It is fascinating to observe how the dispatchable generation sector is pivoting and adjusting to the competition from solar (roof-top and utility scale).

For instance the chart below shows the generation profile of Loy Yang B in January 2020 compared to 2024. In 2020, the power station behaved in the traditional base load station running flat-out at a steady level, and then today, the plant has been able to decrease its minimum generation level and sculpt the generation to try and dodge the solar ‘crushed’ spot price during the day. Life is more complicated for the plant.

As experience has taught us, the first quarter of every year is a story in itself, and 2024 will be another one. We look forward to seeing how the balance of the quarter plays out. We wonder:

- will Victoria have a late summer and the BoM's hot and dry prediction eventuate?

- will we see the Victorian generators buy back and then re-offer capacity at much higher levels

- will Queensland summer now fizzle, or is there more heat to come?

- will Callide C return-to-service before the quarter ends?

Disclaimer and Notes

Energybyte is published by Empower Analytics Pty Ltd (ABN 38630239002), Authorised Representative no 1274453 of Capital Treasury Solutions (AFSL 429066). Any questions or feedback must be directed to Empower Analytics Pty Ltd as the sole publisher.

This newsletter contains general information and is not advice to buy or sell any position.

Empower Analytics has exercised professional care in the preparation of this newsletter, the information includes data from third parties which is not independently verified and it is current at the date of publication. Empower Analytics is under no obligation to update this data.

Before making any trading or investment decision, you should seek professional advice. No liability is accepted for actions or omissions by anyone. Past performance do not predict future outcomes.