As the year approaches an end, we thank all visitors and subscribers to energybyte. We also wish everyone a safe and enjoyable Christmas and New Year. Finally, we recap on market prices over summer, which appear very hot, perhaps too hot and unlikely to be reached.

On behalf of the team at EnergyByte, we wish you and your family all the very best for the Season. We also thought we would quickly review the price outcomes of the current quarter, and the forward price for the pending summer quarter of Q1.

A Year in Review

The year of 2021 will be long remembered as the first year of COVID vaccinations which has allowed the community to emerge from the home castle, and re-engage with each other face-to-face. Not that the battle is over, with Omicron looming and growing in presence.

For energybyte, 2021 was the year we established our digital version of our monthly market report which provides an in-depth analysis of the events of each month, accompanied with a summary of the market energy news each month.

We have also written many one-off articles ranging from:

- Basslink going to voluntary administration

- Market price shocks

- Victorian network tariff changes

- Callide C fallout

- Kurri Kurri Gas Station

- Callide C Catastrophic failure

- Extreme spot prices biting

- Environmental costs surging

- Newport Power Station re-birth

- AGL Split

- Big Batteries - Big Issues

- SA the yellow canary - again

- Origin Energy flexes muscle

- The Big 3 retailers facing more pain

- Forward prices falling

What has happened in Q4?

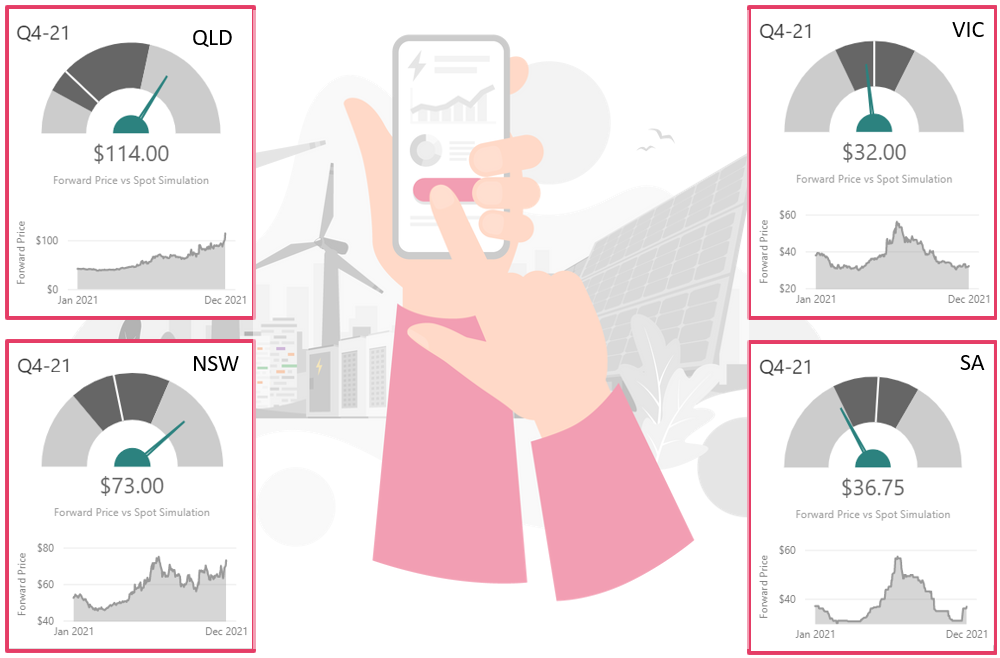

Spot prices for Q4 have been split with QLD and to a lesser extent NSW, taking off while VIC and SA have been more subdued.

We have compared the current Q4 forward price with our probabilistic spot forecast for the same period. The results are shown in the graphic below.

The dials for each State represent our probabilistic spot forecast broken into the four quartiles. The dark green needle represents the forward trading market price at the time of writing this article for the quarter, and reflects the combination of the spot price that has occurred in the past, and the market's expectation for the balance of the quarter.

The results show QLD and NSW forward market Q4 prices are now in the top quartile of the forecast distribution, while VIC is tracking just below the median, and SA in the bottom quartile. The history of the journey of each forward market price since January for each region is shown below each dial.

For a detailed view of recent spot price events we can refer you to WattClarity.

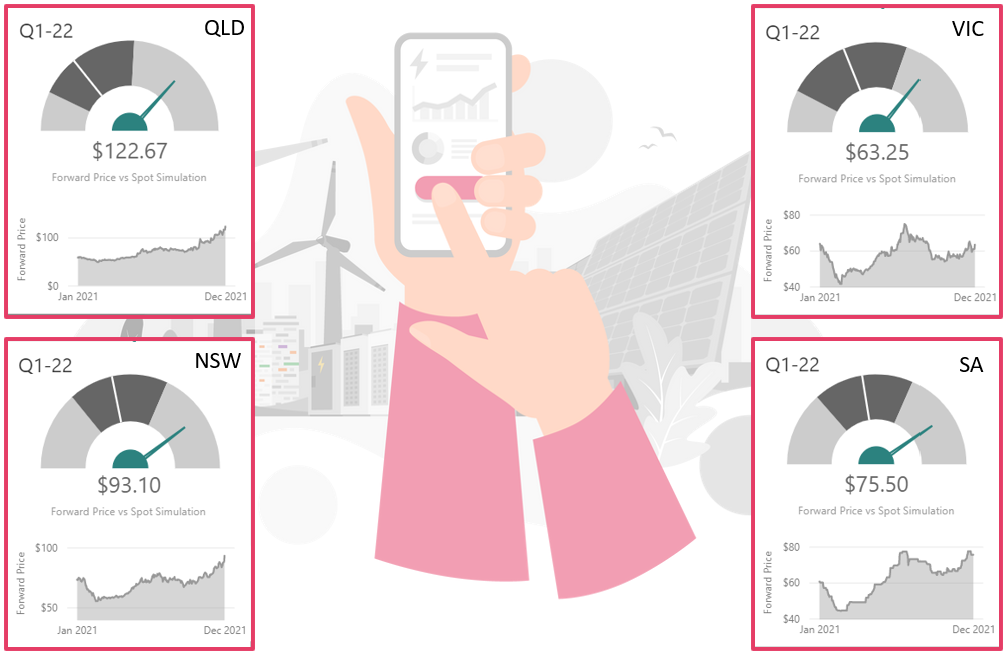

High Expectations for Summer

The market's expectations for summer is super strong across all regions, and according to our modelling is tracking in the top quartile for all regions. This is despite:

- a cooler and wetter weather forecast

- despite more fuel on the ground, a lower bushfire risk

- no shortages in reserve according to AEMO

- more renewable generation coming online, or ramping up

QLD and SA historically have the longest risk tail over the summer quarter, and lead the march to the end of the long-tailed distribution. VIC and NSW are also equally comfortably passed the 75th percentile marker.

It is not uncommon for Q1 to trade above the 75th percentile, but the distance from this marker across all regions, is probably a precedent. Does this mean the market is too hot, and become over-excited? Possibly, and statistically speaking, the odds now suggest that not all price levels will be reached in all Regions. It is more likely some Regions will have a lower price outcome, and less likely, for all Regions to be lower.

Like most markets, the energy trading market is driven by sentiment (and risk management practices). Despite some energy traders wanting to adopt a contrary view of the market, sometimes risk management practices and "What if I am wrong?" dynamics restrict such position taking. For some smaller organisations, the consequence of a cash shock can be fatal.

We look forward to another summer in the industry, as each summer has its own story. Last year, the spot market delivered an outcome in the lowest quartile for all regions except for QLD which was between the 25th and 50th percentile. The results were:

- Tasmania ($34/MWh) having the lowest Q1 average in 10-years

- Queensland ($43/MWh) and Victoria ($25/MWh), the lowest Q1 average in 9-years

- NSW ($38/MWh) and SA ($41/MWh), the lowest Q1 average in 6-years

Once again, last year's Q1 forward market was not a good predictor of actual spot price outcomes. If the forward market price originated from a forecaster in your organisation, they would have been sacked long ago.

If you want to review what happened last summer, you are welcome to browse our March Monthly Report which is our sample report for potential subscribers.

Thank you

Once again we thank our visitors and subscribers to our energybyte platform, and hope you stay safe and enjoy the Festive Season.

During January we will be preparing our Annual Market Report which was our most widely read article.